torm & Tempest Cover Under Fire Insurance – What Is Covered and What Is Not?

by Admin

by AdminWhen strong winds, storms, or severe weather strike, many homeowners assume that any damage caused by the storm will automatically be covered under their Fire Insurance policy.

However, that is not always the case.

👇 Refer to the illustration below

Most standard Fire Insurance policies do not automatically include Storm, Tempest, Hurricane, Cyclone or Windstorm cover.

To obtain this protection, policyholders may need to add Storm & Tempest cover as an extension to their Fire Insurance policy, depending on the insurer and policy wording. Some HouseOwner Insurance policies may already include this coverage.

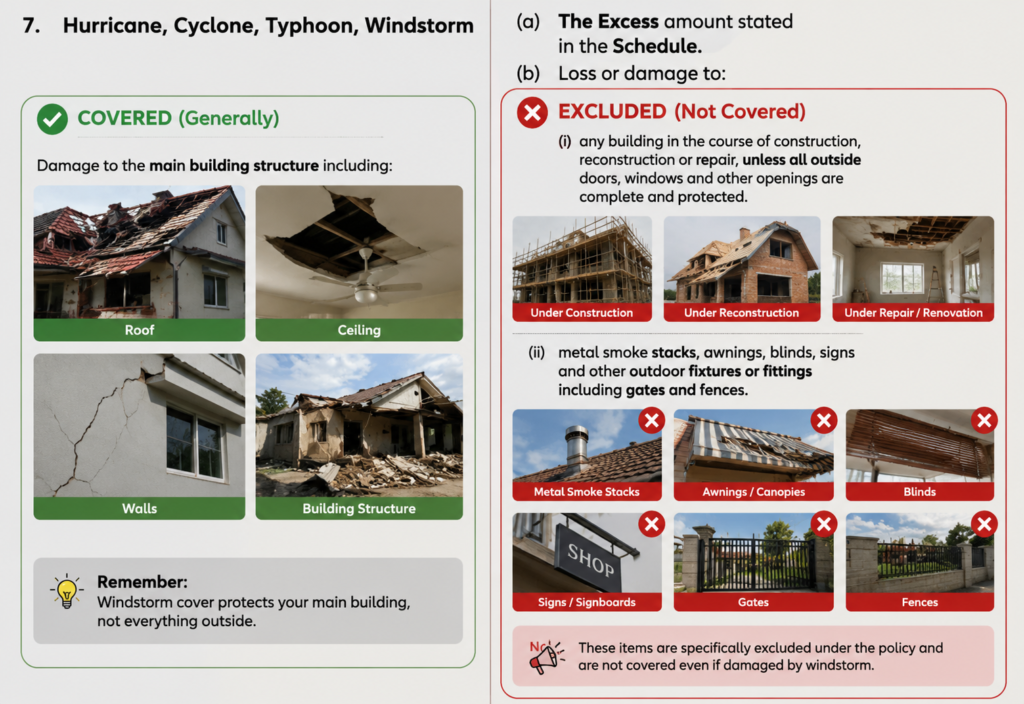

When included, this additional cover generally protects the main building structure against storm-related damage.

✅ Commonly Covered

Damage to the main building structure such as:

- Roof

- Ceiling

- Walls

- Main building structure

For example, if strong winds damage your roof and rainwater enters the house, the resulting damage to the insured building may be claimable, subject to the policy terms, conditions and exclusions.

❌ Common Exclusions

Storm and Tempest cover does not necessarily protect everything located outside the house.

Common exclusions may include:

- Gates

- Fences

- Awnings / Canopies

- Blinds

- Signboards

- Metal smoke stacks

- Buildings under construction, reconstruction or major renovation

These items may require additional coverage or policy extensions, depending on the insurer and policy wording.

💡 Always Check Your Policy Wording

Insurance policies can differ from one insurer to another.

Before assuming that storm damage is covered, it is important to review the policy wording, schedule and any extensions that may apply to your property.

Understanding what is covered — and what is not covered — can help prevent unpleasant surprises when making a claim.

If you are unsure whether your current Fire Insurance policy includes adequate Storm & Tempest protection, speak to your insurance adviser for a policy review.

Not all policies provide the same coverage. Always refer to your policy wording for the exact terms, conditions and exclusions applicable to your insurance policy.

Most homeowners believe burglary only happens to other people.

Most homeowners believe burglary only happens to other people.

Although insurance cannot prevent a burglary from happening, it can help reduce the financial burden when an unfortunate incident occurs.

Although insurance cannot prevent a burglary from happening, it can help reduce the financial burden when an unfortunate incident occurs.