Motor insurance–related content including coverage types, claims experience, common mistakes, and practical tips for vehicle owners to avoid unnecessary losses.

When you’re behind the wheel, you naturally take precautions to protect your family, especially young children. But what if a passenger in your car causes an accident—by opening a door suddenly, distracting the driver, or even unintentionally causing harm to others?

This is where Legal Liability of Passengers (LLOP) comes in—a low-cost add-on to your motor insurance that could save you from major financial loss.

⚠️ Why Is LLOP Important?

Let’s say you’re sending kids to school. One of them suddenly opens the door, and a passing motorcyclist crashes. Injuries happen. You, as the vehicle owner, may be legally liable for what your passengers do—especially if someone is hurt or killed.

Without LLP, you might be sued personally for damages.

💸 The Protection Is Inexpensive—But the Risk Isn’t

LLOP coverage is affordable—often less than the price of a meal

Yet it protects you from tens of thousands in potential legal claims

Especially relevant if you regularly carry children, elderly parents, or other passengers

✅ What LLOP Covers:

Legal liability for death or bodily injury caused by your passengers to other people

Example: passenger opens the car door, causing a cyclist to fall

Applies whether you’re at fault or not—you may still be held responsible as the car owner

🚫 What LLOP Does Not Cover:

Damage caused to your own passengers

Liability when using your car for hire or commercial purposes (unless insured as such)

Deliberate or criminal acts

👨👩👧👦 Real-Life Scenarios

🔹 A child accidentally drops a toy from the window, hitting a motorcyclist

🔹 An elderly parent opens the car door without checking for traffic

🔹 A friend suddenly grabs the steering wheel while joking around

These things happen fast—and without LLOP, the consequences could hit hard.

🛡️ Your Responsibility, Your Peace of Mind

Adding LLOP to your motor policy shows you’re a responsible driver and vehicle owner. It’s about protecting your family—not just in the car, but from legal trouble after the ride ends.

💬 Talk to Us Today

If you’re unsure whether your current policy includes Legal Liability of Passengers, contact us now. We’ll check your coverage, explain your options, and help you stay protected—all without pressure.

A damaged windscreen might seem like a minor issue—until you’re stuck with a costly repair.

In Malaysia, windscreen damage is one of the most common car insurance claims. But it’s important to know: your standard motor policy doesn’t cover it by default. Windscreen protection must be added as a separate benefit.

🔍 What Does Windscreen Insurance Cover?

This optional add-on allows you to claim for the repair or replacement of:

Front windscreen

Rear windscreen

Side windows

Sunroof or moonroof (if installed)

All without affecting your No Claim Discount (NCD).

💡 How It Works

You declare the insured amount based on your car’s glass value

You pay a small additional premium

If the glass breaks, the insurance covers the replacement—up to the insured limit

✅ What’s Typically Covered

Glass damage due to accidents

Chips or cracks from stones or debris

Breakage from attempted theft or vandalism

🔶 Note: Tinting or lamination is not covered unless it is specifically declared and included in the insured amount. 🔺 Excludes: Damage to car body parts or any non-glass components (e.g. sensors, paintwork, wipers).

🔧 What to Expect During a Claim

Most insurers require you to use panel workshops for claims. If you are in Sarawak or other areas without appointed windscreen panels, repairs can still be done—but might take more time and coordination. Always consult your agent before proceeding.

🤔 Is Windscreen Coverage Worth It?

For many car owners, yes. Glass repairs can be unexpectedly expensive, and this add-on helps you manage the cost and keep your NCD intact. It’s a low-cost benefit with high practical value.

📞 Need Help? We’re Here.

At LH Insurance, we’ll help you determine the right insured amount, explain the claim process, and make sure your coverage suits your driving needs—wherever you are in Malaysia.

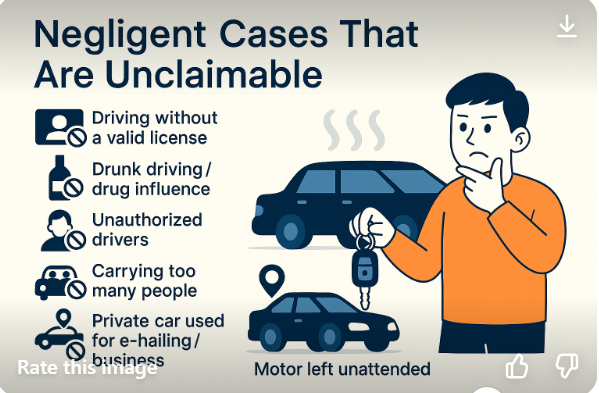

Negligent Cases That Are Unclaimable — What You Must Know Before You Drive

Some accidents may seem minor — but one careless mistake could cause your insurance claim to be completely denied.

We’re not just talking about major crashes or illegal racing. Even small oversights like having an expired license or carrying too many passengers can result in zero payout.

⚠️ Common Situations Where Claims May Be Denied

❌ 1. Driving Without a Valid License

Expired, suspended, or no license at all? Your insurance won’t pay.

❌ 2. Drunk Driving / Drug Influence

If alcohol or drugs are involved, the insurer will void your claim completely — even if the accident was minor.

❌ 3. Unauthorized Drivers

Someone else driving your car without your knowledge?

Unless it’s reported properly and confirmed as theft by the police, you could still be held liable — and your claim may be denied.

❌ 4. Carrying Too Many People

Exceeding the legal passenger limit (e.g. 6 people in a 5-seater)? That alone can void your coverage.

❌ 5. Private Car Used for E-Hailing or Business

Using your private car for Grab, food delivery, or commercial use without declaring it? Your insurer may not cover any damage.

❌ 6. Leaving Your Car Unattended (With Keys Handed Over)

Just because your car was taken doesn’t always mean it qualifies as theft.

Real Case Example: A car owner drove to a car wash and handed his keys to someone he assumed was staff. That person drove off — and the car was never recovered. The insurance company rejected the claim.

Why? Because the keys were handed over voluntarily, and there was no force or break-in, the incident is not considered “theft” under standard motor insurance. It falls under negligence, and is therefore excluded from coverage.

💡 Important Reminder

Never hand over your car keys unless you are 100% sure the person is authorized. If your vehicle is stolen due to your own carelessness, your insurance won’t cover it.

✅ What You Can Do as a Responsible Driver

Keep your license valid

Don’t drink and drive

Follow your car’s legal passenger limit

Don’t allow others to drive without your consent

Declare if your car is used for e-hailing or business

🛡️ Insurance Only Works If You Drive Responsibly

At LH Insurance, we help our clients not just buy insurance — we help them understand it.

Want a quick review to make sure your policy has no hidden gaps? 👉 Contact us today — we’re happy to assist, no obligation.

💬 Final Thought

Insurance is like a safety net — but if the net is torn, it won’t catch you when you fall. Let us help you keep that net strong.

When your car is damaged and needs repairs, sometimes brand new original parts are used to replace old ones. This may leave your car in better condition than before the accident. In such cases, insurance companies may require you to pay a portion of the repair cost — this is called Betterment.

The older your car, the higher the percentage you might have to pay. Here’s a common scale:

Car Age

Betterment You Pay

Less than 5 years

0%

5 years

15%

6 years

20%

7 years

25%

8 years

30%

9 years

35%

10 years and above

40%

❓ What is Waiver of Betterment?

Waiver of Betterment is an optional add-on for your motor insurance that allows you to avoid paying the betterment charges.

✅ With this add-on, the insurer will cover 100% of the cost for new original parts, no matter how old your car is.

💡 Why Choose Waiver of Betterment?

No Extra Charges during repairs using brand new parts.

Peace of mind even if your car is older than 5 years.

You keep more money in your pocket after an accident.

🧮 Example Without Waiver:

Your 7-year-old car needs RM5,000 in repairs.

Betterment rate = 25%

You pay: RM1,250

Insurance pays: RM3,750

🧮 Example With Waiver:

Same scenario, but you have Waiver of Betterment.

You pay: RM0

Insurance pays: RM5,000

📝 How to Add Waiver of Betterment?

Available for Comprehensive Private Car policies only.

Car must be within 10 years old.

Add it when you renew or purchase your insurance.

🌟 Drive smarter, save more — ask us about Waiver of Betterment today and enjoy full protection without hidden costs!

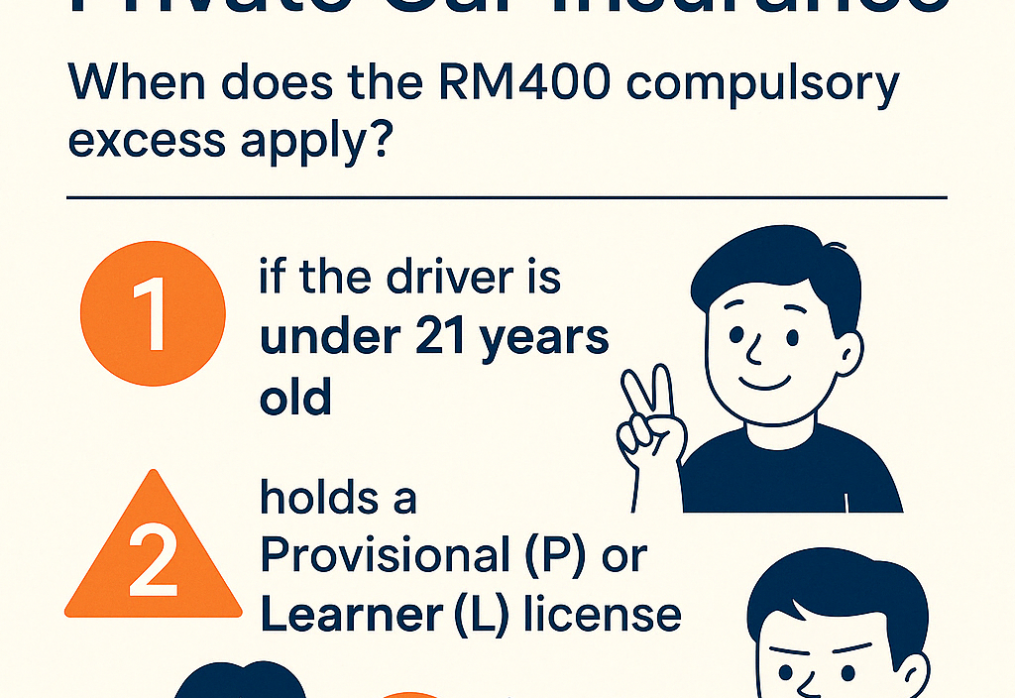

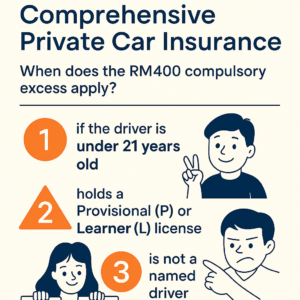

If you ever need to make a car insurance claim, excess is the portion of the cost that you, the policyholder, have to pay first before your insurer covers the rest.

Now here’s the twist: There’s something called “Compulsory Excess” – an additional RM400 you must pay under specific conditions, no matter how good your driving record is.

🚨 When Does the RM400 Compulsory Excess Apply?

This additional charge kicks in if the driver involved in the accident meets any of the following:

1️⃣ Under 21 years old

Young and adventurous? Yes. But also, statistically riskier.

2️⃣ Holds a Provisional (P) or Learner (L) license

These are beginner drivers still under training.

3️⃣ Not named in your policy as a “Named Driver”

If someone drives your car but their name is not listed in your insurance, this rule applies—even if they’re fully licensed.

📷 Refer to this infographic for a quick summary:

👉

💰 Example: How It Affects Your Claim

Let’s say a claim is RM3,000:

If compulsory excess applies, your insurer pays RM2,600, and you pay RM400.

If not applicable, insurer pays the full RM3,000. You pay RM0.

✅ How to Avoid Paying This Excess?

Name additional drivers in your policy (especially children or spouse).

Make sure they’re over 21 and fully licensed.

Consider adding a Compulsory Excess Waiver if your insurer offers it.

📜 Straight From the Policy:

“We have the right to deduct RM400 if the driver is under 21, holds a P or L license, or is not named as a driver in your schedule.” (Source: Allianz & Generali Private Car Policy Wording)

👀 Final Thought

Most people only learn about “compulsory excess” after an accident. Don’t be one of them. Review your policy today—or better, let us review it for you.

If your vehicle suddenly refuses to move—don’t panic. Most comprehensive private car insurance policies in Malaysia offer free towing to help you get out of trouble.

This isn’t just a nice bonus. It’s a practical benefit that can save you hundreds and a lot of stress when you need it most.

✅ What Does the Policy Say?

According to Allianz’s Private Car Policy and Takaful contracts from companies like Etiqa:

Towing costs are covered (up to RM200) if your vehicle is undriveable due to insured damage and needs to be moved to:

by Admin

by Admin